Building Sector Coupling: Making Existing Stock Profitable

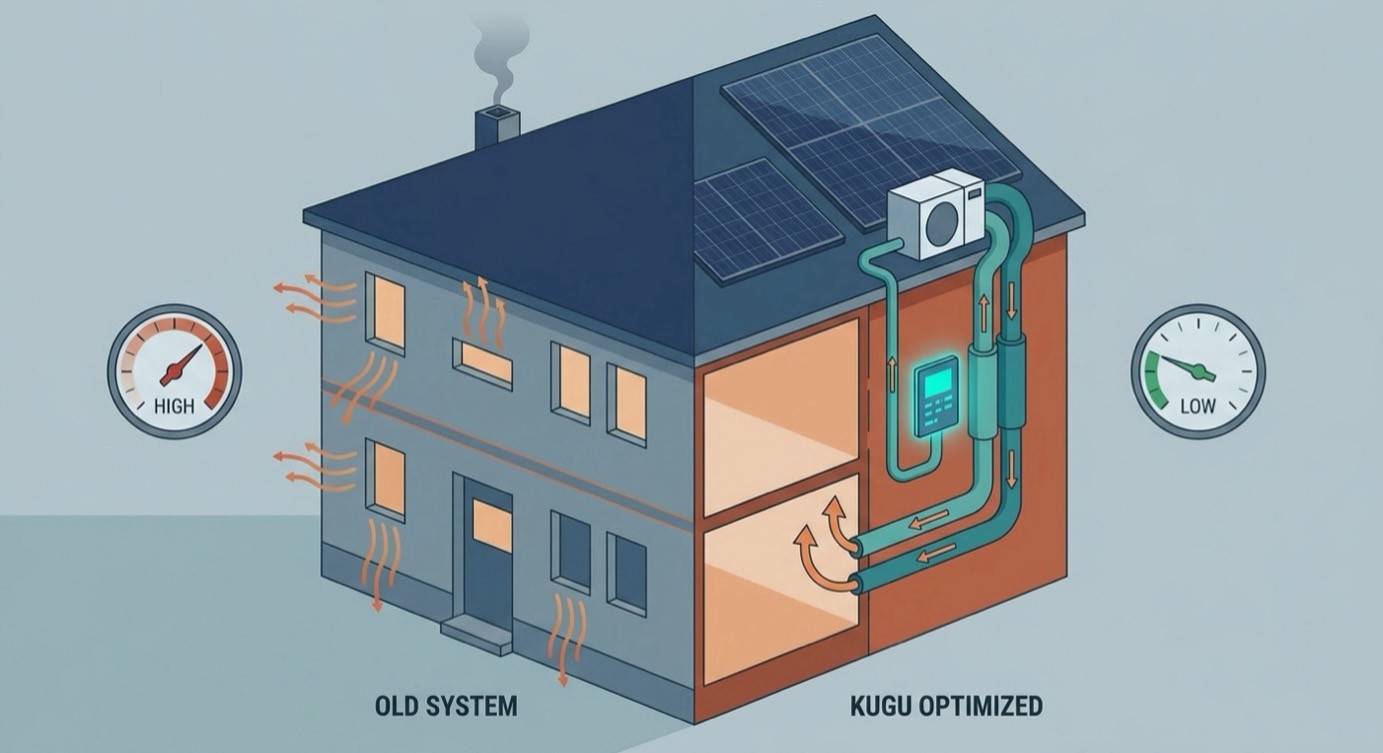

Sector coupling in buildings brings the heat side and the power side into one controlled operation: heat pump, buffer and battery storage, local PV generation and dynamic electricity prices all interact, even in existing stock. The economic value shows up where heat generation, storage and price signals actually come together in a way you can control. Installing new equipment alone does not get you there.

For housing companies, this is less a question for new builds than one of operational management in the existing portfolio. New buildings already heat mostly with electricity, while the residential stock still runs heavily on fossil fuels. That is exactly why coupling becomes a transformation task spanning entire portfolios. What matters in the end is not the individual system, but a clear question: which buildings can you control, measure and assess economically?

Before a portfolio strategy takes shape, it pays to look at the tension between coupling potential and the control you actually have in existing stock.

- Coupled sectors in the boiler room: flow and return temperature, volume flow, storage level and tariff data make electricity and heat controllable.

- Economics come from operation: load shifting, more efficient heat pump operation and early fault detection carry the business case more than new hardware.

- Suitability follows controllability: without storage capacity, remote control and data access, the value of dynamic electricity prices stays limited.

- Verifiability as an ESG lever: only measurable energy and CO₂ impact at portfolio level becomes reportable.

How does sector coupling make buildings more economical?

Sector coupling in a building becomes economical when heat generation, electricity purchase, storage and price windows work together as one controllable operation. Blanket payback promises will not help you here. The strongest business case comes from combining lower final energy, more efficient heat generation, shifted electricity loads, less faulty operation and reliable transparency. New technology alone does not deliver that. The control layer on top of it does.

Which sectors interact?

In the boiler room, the heat pump is what directly couples the electricity and heat sectors. Around it, buffer storage, domestic hot water storage, local PV generation and, optionally, a battery work together, all steered by heat demand, weather forecast and price signal. A heat pump only becomes economically optimisable once it no longer just runs, but is controlled according to demand, storage level, electricity price and comfort limits. This control is where coupled technology turns into coupled operation.

Where do the savings levers come from?

Since 2025, all electricity suppliers have been required to offer dynamic electricity tariffs, which pass on the price movements of the day-ahead and intraday markets in short intervals. For a large consumer like a heat pump, that creates a new optimisation lever, as long as the building can store heat for a while. The Bundesnetzagentur's modelling shows that since April 2025, dynamic prices have consistently stayed below modelled fixed-price tariffs.

The real value lies in avoiding high-price windows and using low-price ones, without losing transparency in operation. A hands-on example is the EOS Strompreisdynamik mode (EOS stands for Energie-Optimierungssystem), which brings heat demand, dynamic prices, heat pump, buffer storage, PV and battery together on a 15-minute cycle. As a company figure, KUGU states an average saving potential of more than 20 percent and a guaranteed saving of 12 percent.

- Load shifting: heat production moves into cheap electricity windows when storage bridges the time gap.

- More efficient heat pump operation: demand-driven control lowers final energy and avoids inefficient operating points.

- Transparency and diagnosis: faulty operation caught early saves energy and maintenance costs across the portfolio.

For existing systems, the consequence is clear: without thermal storage capacity and remotely controllable regulation, the economic value stays limited. Flexibility only emerges with a buffer that respects comfort and hygiene limits.

When is sector coupling worthwhile in existing buildings?

In existing stock, sector coupling pays off first where electricity-based heat generation, storage capacity, data access and controllable operation come together. Strong candidates are buildings with a central heating plant, a heat pump or hybrid system, existing storage, PV potential and recurring operational anomalies. That heat pumps work measurably in existing buildings is documented by Fraunhofer ISE.

In its completed research project, the institute studied 77 heat pumps in existing buildings. Air-to-water systems reached an average seasonal performance factor of 3.4, ground-source systems 4.3. The range from 2.6 to 5.4 makes it clear how strongly design and operation decide the economics. These values come mostly from single- to three-family homes. For large multi-family portfolios they point the way, but they cannot be transferred one to one.

- Central heating plant with high consumption: bundles the heat load and makes optimisation scalable.

- Heat pump or hybrid system: couples electricity and heat and creates the basis for load shifting.

- Existing storage: buffer, domestic hot water or building mass allow flexibility over time.

- PV potential on the building: raises self-consumption, especially when coupled with the heat pump.

- Remotely readable meters and data access: deliver the operating data for assessment and control.

Worth knowing: The dena practical guide for heat pumps in multi-family buildings addresses the strategic and technical departments of housing companies directly and deals with system solutions for existing stock.

There are also clear counter-cases. If there is no electricity-based heat generation, no relevant storage capacity, no way to control the system remotely, or the operation is already running at its comfort and temperature limits, then monitoring and basic optimisation come before any dynamic electricity price logic. In these buildings, transparency pays off first, before price windows become usable at all.

Which data makes buildings controllable?

A building becomes controllable through measurable operating data, not through general digitalisation. An economic assessment needs at least flow and return temperature, volume flow, heat output, heat quantities, the heat pump's electricity consumption, outdoor temperature and weather forecast, operating states, storage level, plus tariff and price data. Only these points separate a solid assessment from bare annual consumption figures.

Three data worlds belong cleanly apart. Electricity data from the intelligent metering system is the prerequisite for using dynamic tariffs in the first place. Heat data such as heat quantities, COP and efficiency ratio per generator assesses system efficiency. And operating data from the control layer is what makes steering possible at all, the way KUGU VIS (VIS stands for Visuelles-Informationssystem) and VIS Anlagendiagnose make it visible in real-time monitoring.

- Electricity side for tariffs: iMSys meter data and price curves for dynamic control.

- Heat side for system assessment: heat quantities, COP, efficiency ratio and energy contribution per generator.

- Operating side for control: temperatures, volume flow, storage level and operating states.

With the smart meter rollout, though, there is a gap that directly affects many portfolios. Among those with a mandatory rollout are final consumers above 6,000 kWh annual electricity consumption, as well as controllable systems under §14a EnWG, which include heat pumps. According to the Bundesnetzagentur's assessment for the fourth quarter of 2025, only 23.3 percent of mandatory installation cases between 6,000 and 100,000 kWh per year were fitted with an iMSys. We describe the digital groundwork for this in more detail in our article on connected heating systems.

In practice, this leads to the decisive question: which data is missing first? If the electricity side is missing, dynamic price optimisation is blocked. If the heat side is missing, you cannot prove system efficiency and cannot properly justify an investment decision.

Which hurdles slow existing buildings down?

Existing stock is usually held back by technical constraints, data gaps and unclear responsibilities. According to the practical guide from dena, Fraunhofer ISE and GdW, multi-family buildings are far more complex than single-family homes, because domestic hot water, heat sources, installation space, noise, hydraulics, higher outputs and the user structure all come into play at once. In practice, domestic hot water and hydraulics weigh the heaviest, because high flow temperatures and rigid distribution directly limit efficiency. On top of that come missing operating data and unclear operator, owner and tenant roles, which make clean billing under §7 of the German Heating Costs Ordinance harder. Anyone who skips these hurdles and aims straight for dynamic electricity prices is simply setting the wrong priorities.

How do housing companies prioritise portfolios?

Prioritisation runs through the combination of decarbonisation pressure, cost risk and data availability. The building sector caused around 100 million tonnes of CO₂ equivalents in 2024, while the national emissions trading system makes fossil heat more expensive in 2026 within a corridor of 55 to 65 euros per tonne. At the front of the queue, then, are buildings with high consumption, a controllable system and available data, because they make measurable value scalable. On the regulatory side, as of July 2026 the uniform 65 percent renewable energy requirement is applicable law, and its replacement exists as a cabinet draft for the Building Modernisation Act (Gebäudemodernisierungsgesetz). For portfolio transparency, our digital energy platform offers the right orientation.

The next lever in existing stock

Sector coupling in buildings unfolds its value as an operational capability, carried by digital transparency and a decarbonisation approach thought through in economic terms. A single technology project does not deliver this. It takes the ability to steer and prove heat, electricity, storage and price signals over the long term through measurable data.

Three points stay central for decision-makers. Controllability is the prerequisite, because without storage capacity, remote control and data access, any coupling remains theory. Economics come from operation, from shifted loads, efficient generation and faulty operation caught early. And scaling only succeeds with measurable building data that makes energy and CO₂ impact reportable at portfolio level.

The concrete next step is a portfolio pre-selection: identify suitable buildings by data availability and system type, analyse how the candidates actually run, and pilot the coupling at selected sites before rolling it out across the entire stock.

Frequently asked questions (FAQ)

Does sector coupling in buildings always have to start with a heat pump?

No. A heat pump or hybrid system is the strongest coupling core, because it directly connects electricity and heat. If one is not yet in place, it pays to start with a transparency phase of monitoring and basic optimisation. Without a sufficient data basis, storage capacity and controllable operation, dynamic electricity price optimisation brings little benefit.

Which existing buildings are suitable for sector coupling first?

The first candidates are buildings with a central heating plant, high consumption, a heat pump or hybrid system, existing storage, PV potential and recurring operational anomalies. Remotely readable meters and data access matter just as much. Suitability depends not only on the technology, but also on usable flexibility through thermal storage capacity.

What do dynamic electricity prices offer for heat pumps in multi-family buildings?

Dynamic electricity prices shift heat pump operation into cheap electricity windows and avoid expensive high-price phases. Since 2025 such tariffs have been a mandatory offering, and the Bundesnetzagentur's modelling has stayed below fixed-price tariffs since April 2025. The benefit only emerges with storage capacity and controllable regulation, though. Guaranteed savings cannot be promised independently of the specific building.

Which measurement data does sector coupling in buildings need?

You need at least flow and return temperature, volume flow, heat output, heat quantities, the heat pump's electricity consumption, outdoor temperature and weather forecast, operating states, storage level, plus tariff and price data. On the electricity side, an intelligent metering system is the prerequisite for using dynamic tariffs at all and for assessing operation economically.

Why is PV alone not enough in existing stock?

PV is a valuable building block, but it does not cover the heat demand on its own. In winter, high heat demand and low PV generation drift apart, which is why storage, tariffs and control stay decisive. On rented multi-family buildings, PV becomes more economically attractive when it is coupled with the heat pump, so more electricity is consumed directly on site.

How does sector coupling affect heating cost billing and verifiability?

Sector coupling calls for a clean separation of electricity, heat and consumption data. Under §7 of the Heating Costs Ordinance, electricity consumption, heat quantities and consumption metering are particularly important for auditable billing with heat pumps. For ESG purposes, coupling only becomes reportable once energy and CO₂ impact are available in a measurable, plausibility-checked and documented form at building or portfolio level.